Home Insurance Costs Killing Your Deal? Here's What Chattanooga Buyers Need to Know Before They Make an Offer

Chattanooga Robert Wills March 2, 2026

Chattanooga Robert Wills March 2, 2026

You found the house. Made a solid offer. Got your financing lined up. Then a week before closing, your insurance quote comes back $150 higher per month than you expected. Suddenly, your debt-to-income ratio is too high, and your lender is backing out.

This scenario is happening more often in 2026, and it is catching buyers off guard across the Tennessee Valley and North Georgia. Home insurance costs have climbed steadily over the past few years, and they are no longer just a line item you can ignore until the last minute.

If you are buying a home in Chattanooga, Ringgold, Ooltewah, or anywhere in Hamilton County or Catoosa County, you need to factor insurance into your budget before you make an offer: not after.

When your lender calculates how much house you can afford, they look at your debt-to-income ratio. That is your total monthly debt payments divided by your gross monthly income. Your mortgage payment includes principal, interest, taxes, and insurance. If your insurance quote comes back higher than expected, it increases your total monthly housing payment, which can push your DTI ratio over the limit your lender allows.

In Chattanooga, the average homeowner pays about $232 per month for home insurance. That comes out to roughly $2,784 per year. That is actually about 8% below the national average, which is good news. But here is the catch: actual costs can range anywhere from $305 to $2,949 per month depending on your home, your credit score, and the coverage levels you need.

If you budgeted for $200 per month and your quote comes back at $300, that is an extra $1,200 per year you did not plan for. And if you are already close to your DTI limit, that extra $100 per month could be the difference between getting approved and having to restart your home search.

Several factors will affect your final insurance quote, and many of them are tied directly to the condition of the home you are buying.

Credit score is a big one. In Tennessee, buyers with poor credit pay an average of $6,060 annually for home insurance. That is 113% more than buyers with good credit. If your credit is not where you want it to be, expect higher premiums.

Coverage levels also matter. Most insurance quotes are based on $250,000 to $300,000 in dwelling coverage. If you are buying a larger or more expensive home, you will need more coverage, which means higher premiums.

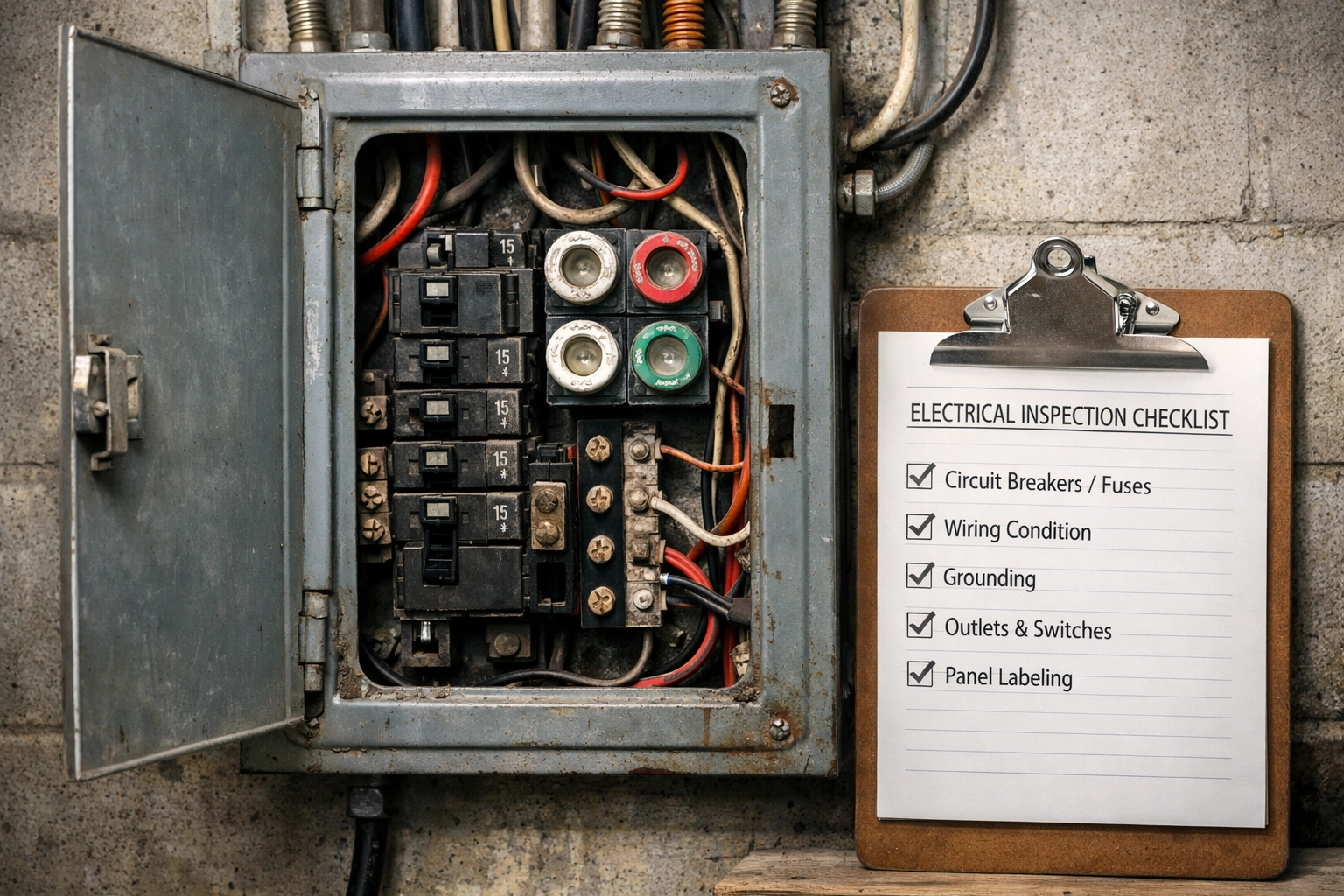

But the factors that catch most buyers off guard are the ones tied to the home itself: the age and condition of the roof, the electrical panel, the HVAC system, and the plumbing. These are the big-ticket items that insurance companies care about because they represent the biggest risk.

Insurance companies do not want to cover homes that are one storm away from filing a major claim. If the roof is 20 years old and looks like it might not survive the next hailstorm, your insurer is either going to charge you a lot more, require you to replace it before closing, or refuse to cover the home at all.

The same goes for outdated electrical panels, especially older fuse boxes or aluminum wiring. These are fire hazards, and insurers know it. If the home you are buying has an outdated electrical system, you need to know that before you make an offer: not when you are trying to secure insurance two weeks before closing.

Here is what you should do: as soon as you get into the inspection period, ask your home inspector to pay close attention to the roof, the electrical panel, the HVAC system, and the plumbing. Get a sense of how old these systems are and whether they will cause issues with insurance. If the roof is 15 to 20 years old, plan on replacing it soon. If the electrical panel is outdated, factor in the cost of an upgrade.

Knowing this information early gives you options. You can negotiate with the seller to replace the roof or update the electrical before closing. Or you can budget for those expenses and adjust your offer accordingly. What you do not want is to find out about these issues when it is too late to do anything about them.

Most buyers wait until they are a week or two away from closing to get serious about insurance. That is a mistake.

You should start reaching out to insurance agents as soon as your offer is accepted. Ideally, you want to have multiple quotes in hand before your inspection period ends. This gives you time to shop around, compare rates, and identify any red flags with the property that might drive costs up.

If you wait until the last minute and find out that the only company willing to insure the home wants $400 per month, you are stuck. You either pay the higher premium and hope your lender approves the higher DTI ratio, or you walk away from the deal and lose your earnest money.

Getting quotes early also gives you leverage. If your inspection reveals that the roof needs replacing or the electrical panel is outdated, you can use that information to negotiate with the seller. You can ask them to handle the repairs, or you can request a credit at closing to cover the costs. But you can only do that if you know about the issues early enough.

Standard home insurance policies in Tennessee do not typically cover flood damage. If you are buying a home near the Tennessee River, Chickamauga Creek, or in areas of Chattanooga, East Ridge, or Red Bank that are prone to flooding, you may need a separate flood insurance policy.

Flood insurance is offered through the National Flood Insurance Program, and the cost depends on your home's flood zone designation. If the home you are buying is in a high-risk flood zone, your lender will require flood insurance. Even if it is not required, it may still be worth considering, especially if the home is near water.

Wind and hail damage are typically covered under standard policies, but you should confirm that with your insurance agent. Chattanooga and the surrounding areas do see severe storms, and you want to make sure your policy covers the types of damage that are most likely to happen.

At Robert Wills Properties, we work with buyers every day who are navigating these exact challenges. Our team of agents have helped hundreds of clients close on homes across the Tennessee Valley and North Georgia areas, and we know how to spot potential insurance issues before they become deal-breakers.

When you work with us, we will walk you through the entire buying process, including when to get insurance quotes, what to look for during inspections, and how to negotiate with sellers when big-ticket items need attention. We have relationships with local inspectors and insurance agents who can help you get the information you need quickly.

We also make sure you understand how insurance costs will affect your monthly payment and your debt-to-income ratio before you make an offer. That way, there are no surprises at the closing table.

Whether you are buying in Ooltewah, Ringgold, Signal Mountain, or anywhere else in the region, our goal is to make sure your transaction is smooth from start to finish.

If you are in the market for a home, here is what you should do:

1. Build insurance into your budget from day one. Use the $232 per month average as a starting point, but understand that your actual costs could be higher depending on the home and your credit score.

2. Get insurance quotes as soon as your offer is accepted. Do not wait until the last minute. Reach out to multiple insurance agents and get quotes based on the specific property you are buying.

3. Pay attention to the roof, electrical panel, HVAC, and plumbing during your inspection. These are the systems that will impact your insurance costs the most. If they are outdated or in poor condition, plan accordingly.

4. Talk to your lender about how insurance costs will affect your DTI ratio. Make sure you understand how much cushion you have in your budget before you commit to a home.

5. Work with an experienced agent. Buying a home is complicated, and insurance is just one piece of the puzzle. Having someone on your side who knows the local market and understands how to navigate these issues can save you time, money, and stress.

If you are ready to start your home search or if you have questions about insurance costs and how they might affect your purchase, reach out to Robert Wills Properties. We are here to help you make smart decisions and close on the right home with confidence.

You can reach us at robertwillsproperties.com or give us a call. We are looking forward to working with you.

Chattanooga

Don't let rising premiums sneak up on you at the closing table.

Chattanooga, TN

A guide to the unique lifestyles and communities that make the Tennessee Valley feel like home.

Chattanooga

ore options, less frenzy. Here’s how to navigate the Tennessee Valley’s growing inventory this season.

Chattanooga

A deep dive into the trends, prices, and inventory shaping the Tennessee Valley this year.

Chattanooga

Smart financial moves for buyers navigating the 2026 Chattanooga market.

Chattanooga

Navigating the 2026 market and interest rate reality in the Tennessee Valley.

Chattanooga

Finding the perfect spot for your family to grow in the Tennessee Valley.

Chattanooga

Discover what’s driving the buzz and how you can benefit from the Tennessee Valley’s new real estate landscape.

Local

Unlock the selling secrets local homeowners are using to stand out—and cash in—this year.

Work with a dedicated real estate professional with deep roots in Chattanooga, who combines local expertise, a passion for client satisfaction, and cutting-edge technology to make your home-buying experience seamless and stress-free.